👛 Stablecoins & payments in Africa

Ahead of our 2nd set of virtual intimate roundtables for African crypto leaders ,we are sharing a high-level overview of the topic of conversation!

You can find the key learnings from our last roundtable, focused on exchanges in Africa here.

Crypto's killer application is stablecoins, and this statement is more factual in Africa and other emerging markets than anywhere else. In fact, the recent Chainalysis crypto adoption report found that stablecoins accounted for 50%+ of crypto volumes in Africa. Stablecoins offer Africans cheaper international money transfers (remittances or for businesses) and also a way to protect their assets from value erosion that would have otherwise happened if they were saving in their local currencies, which are very volatile.

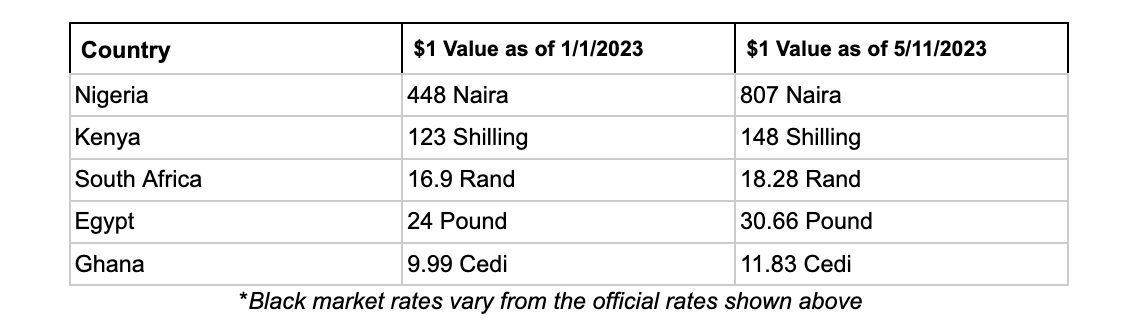

FX Shortage and Currency Devaluation in Africa

Many emerging markets such as those in Africa face challenges with FX shortage (especially USD) which has resulted in limits on local access to FX. For example, Nigerian banks have spending limits on Nigerian bank cards when making International payments. This means users cannot spend their money and pay for international services, which arguably has been a key driver of the initial success of neobanks with their virtual USD cards. With foreign debt rates rising for many African countries this trend of FX shortages is only likely to increase.

Further FX shortages and high inflation is causing African currencies to devalue.

Stablecoins have become an integral part of doing business across Africa. Every day, individuals and businesses alike use it as a hedge or as a saving vehicle to protect their wealth. Companies use stablecoin to send payments to merchants, family members use stablecoins for remittance purposes, and these use cases are just the start.

Stablecoins potential

Hedging & saving:

According to a report by the rest of the world, In Zimbabwe, private savings clubs and amateur investors are looking to crypto and opting for stablecoins as the safer option, according to a vice chair of a Harare-based club that runs a savings program for informal traders in US dollars and other currencies, by converting the club funds from the local currency into stablecoins, it hedges against value loss, especially with volatile currencies such as the Zimbabwe dollar.

This behaviour is mirrored across the continent by individuals as well as a growing number of businesses.

Remittances:

Remittance to Africa has doubled over the last decade, reaching up to $100 Billion in 2022. This surpasses the funds received via Foreign Direct Investment(FDI) and is a huge percentage of most African countries. Despite this, Africa has one of the highest costs of receiving remittance payments.

According to a World Bank report, the average cost of sending $200 to Africa was 8.5% compared to less than 6% globally. Sending money to some African countries can cost as much as 20%, with numerous frictions along the way. Stablecoins have helped some of this issue, as sending payments cost is very low compared to the traditional offerings.

Foreign trade:

Much like for remittances, it is expensive and at times unreliable to send money internationally and between countries within Africa. Stablecoins are also heavily used for commercial trade across Africa; importers and traders, especially the ones that do business with Asian countries, have turned to using stablecoins as the primary mode of payment.

Similarly, most OTC desks across Africa also use stablecoins to move money across borders for clients. This has become a lucrative business, and numerous startups and businesses have sprung up to build products that serve those needs.

PAPSS (The Pan-African Payment and Settlement System)

PAAPS can be described as the SWIFT of Africa. PAPSS wants to enable the efficient flow of money across African borders. PAPSS collaborates with African central banks to provide a payment and settlement service to which commercial banks, payment service providers, and fintechs across the region can connect as participants.

The objective of PAPPS is to provide a single payment infrastructure that cuts through the existing challenges of local currency exchanges across Africa, such as the high cost of cross-border transfer and slow settlement time. With promises of near instant payments (with 120seconds) if successful PAPSS alongside the likes of the AfCFTA (African Continental Free Trade Area) could boost intra African trade from its current levels of accounting for 14.4% of African exports

Enjoyed this article? Don’t forget to share Emerging Onchain with others …